The collapse of Enron in 2001 wasn’t just a corporate bankruptcy; it was a seismic event that shattered public trust, vaporized billions in shareholder wealth, and exposed a dark underbelly of corporate greed and accounting malfeasance. This wasn’t a simple case of a company making a few bad bets. Enron’s downfall was a meticulously crafted illusion, a house of cards built on a foundation of deception, intricate financial engineering, and a culture of unchecked ambition that ultimately consumed itself. What makes the Enron story so compelling, even decades later, is its enduring relevance as a cautionary tale about the seductive nature of unchecked ambition and the catastrophic consequences of prioritizing profit above all else. The question remains: How did a company once hailed as a beacon of innovation become a symbol of corporate corruption?

From Humble Beginnings to Energy Titan: The Meteoric Rise of Enron

Enron’s story began in 1985, born from the merger of two relatively obscure natural gas pipeline companies: Houston Natural Gas and InterNorth. Under the leadership of Kenneth Lay, a charismatic and politically connected executive, Enron embarked on a radical transformation. The company quickly capitalized on the wave of energy deregulation sweeping the United States, pivoting from a traditional pipeline operator to a sophisticated energy trader. This wasn’t just about moving gas from point A to point B. Enron pioneered the concept of trading energy futures and derivatives, creating complex financial instruments that allowed businesses to hedge against price fluctuations in the volatile energy markets.

Enron’s innovative approach wasn’t limited to trading. The company aggressively expanded into new markets, including electricity, broadband, and even water trading. They envisioned themselves as a “market maker” in virtually any commodity, leveraging their trading expertise and sophisticated technology to create new markets and generate massive profits. At the time, this strategy seemed revolutionary.

The Illusion of Prosperity: Enron’s Dazzling (and Deceptive) Financial Performance

By the late 1990s, Enron was a Wall Street darling. Its stock price soared, and the company consistently reported record profits. Enron was lauded by Fortune magazine as “America’s Most Innovative Company” for six consecutive years, from 1996 to 2001. Executives like Kenneth Lay and Jeffrey Skilling were celebrated as visionary leaders, and Enron was held up as a shining example of the “new economy” – a dynamic, fast-growing company that was rewriting the rules of business.

However, this impressive performance was, in large part, a meticulously constructed illusion. Behind the scenes, Enron was engaging in a complex web of accounting fraud and financial manipulation designed to hide its mounting debt and inflate its profits. To maintain the image of constant growth and profitability, the company needed to keep hitting ever-more-ambitious targets. This created a pressure-cooker environment where unethical practices became normalized and even encouraged.

The Cracks Appear: Mark-to-Market Accounting and the Art of Hiding Debt

One of the key tools in Enron’s arsenal of deception was its aggressive use of “mark-to-market” accounting. While technically a legitimate accounting method, mark-to-market allowed Enron to book the estimated future profits from long-term contracts as current income, even if the actual cash flow wouldn’t materialize for years, or worse, might never be realized.

Imagine signing a 10-year contract to sell natural gas at a fixed price. Under mark-to-market, Enron could immediately recognize the entire anticipated profit from that contract, even if the gas hadn’t been delivered and the payment was years away. This created a dangerous disconnect between reported earnings and actual cash flow.

For example, if Enron estimated a contract would generate $10 million in profit over its lifetime, they could book that entire $10 million as income in the first year, even if they only received $1 million in actual revenue that year.

In the short term, this inflated profits and fueled the company’s stock price. However, it also created a dangerous dependency on future performance. If those estimated future profits didn’t materialize, Enron would be left with massive liabilities and no corresponding revenue to cover them. In essence, they were counting chickens before they hatched, and then counting them again. This practice created a dangerous feedback loop: the higher the stock price went, the more pressure there was to find new deals and book even more future profits, regardless of their actual viability.

Special Purpose Entities (SPEs): The Black Holes of Enron’s Balance Sheet

To further conceal its debt and manipulate its financial statements, Enron created a network of thousands of “special purpose entities” (SPEs). These were ostensibly independent companies that Enron used to park its debt and risky assets, effectively hiding them from investors and analysts. However, many of these SPEs were controlled by Enron executives, creating a clear conflict of interest. They were often used to conduct transactions with Enron at inflated prices, further boosting Enron’s reported profits.

A prime example of this manipulation was the “Raptor” entities. These were a series of SPEs created by Enron’s Chief Financial Officer, Andrew Fastow, designed specifically to absorb Enron’s troubled assets and liabilities. They were funded in part by Enron’s own stock, creating a house of cards that was destined to collapse. The raptors were meant to be independent, but Fastow himself managed them, receiving millions in management fees. The conflict of interest was blatant, but at the time, no red flags were raised.

The House of Cards Collapses: Enron’s Descent into Bankruptcy

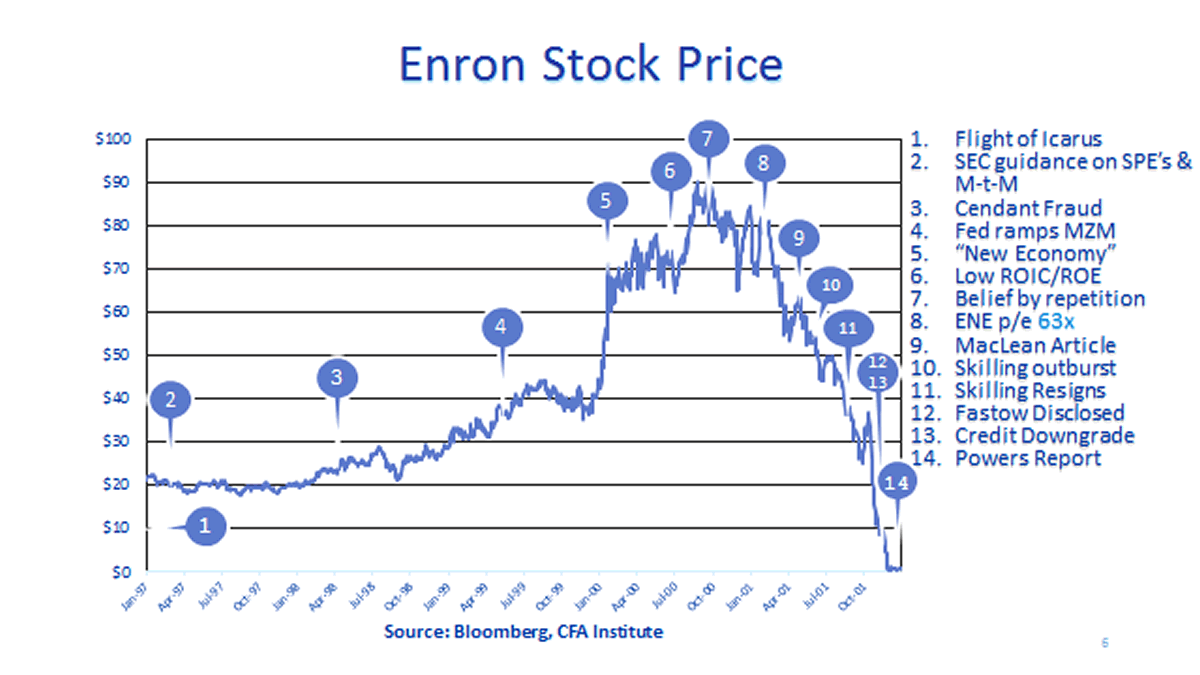

By the summer of 2001, the cracks in Enron’s carefully constructed façade began to widen. Analysts started questioning the company’s complex financial statements and the opaque nature of its SPEs. Whispers of accounting irregularities began to circulate. A few brave journalists, notably Bethany McLean of Fortune magazine, began to dig deeper, exposing the rot at the heart of Enron’s empire. In her seminal article “Is Enron Overpriced?” published in March 2001, she questioned the company’s ability to sustain its high growth rate and the lack of transparency in its financial reporting. In August 2001, Jeffrey Skilling abruptly resigned as CEO, citing “personal reasons.” This unexpected departure sent shockwaves through the market and fueled further speculation about Enron’s financial health. The company’s stock price, which had peaked at over $90 per share in 2000, began a precipitous decline.

In October 2001, Enron announced a massive $638 million loss for the third quarter and revealed that it had overstated its profits by nearly $600 million over the past four years. The company also disclosed that it had reduced shareholder equity by $1.2 billion due to accounting errors related to its SPEs.

The revelations triggered a full-blown panic. Investors fled, and Enron’s stock price plummeted to pennies. Credit rating agencies downgraded Enron’s debt to junk status, making it impossible for the company to raise new capital. On December 2, 2001, Enron filed for Chapter 11 bankruptcy, one of the largest in U.S. history at the time. Thousands of employees lost their jobs and their retirement savings, which were heavily invested in Enron stock. The value of the company was wiped out, and Enron’s shareholders were left with nothing.

The Aftermath: Justice Served (to a Degree) and Lasting Reforms

The Enron scandal sent shockwaves through the corporate world and led to a wave of investigations, lawsuits, and regulatory reforms. Several Enron executives, including Kenneth Lay, Jeffrey Skilling, and Andrew Fastow, were indicted on charges of fraud, conspiracy, and insider trading.

- Kenneth Lay was convicted on multiple counts of fraud and conspiracy but died of a heart attack before he could be sentenced.

- Jeffrey Skilling was convicted of 19 counts of fraud, conspiracy, insider trading, and making false statements to auditors. He was sentenced to 24 years in prison but was released early in 2019 after serving 12 years.

- Andrew Fastow, the architect of many of Enron’s fraudulent schemes, pleaded guilty to two counts of conspiracy and served six years in prison. He also agreed to cooperate with prosecutors and testify against other Enron executives.

The Enron scandal also led to the demise of Arthur Andersen, one of the “Big Five” accounting firms, which had served as Enron’s auditor. Arthur Andersen was convicted of obstruction of justice for shredding documents related to its audits of Enron. The conviction was later overturned by the Supreme Court, but the firm’s reputation was irreparably damaged, and it ceased operations.

The Sarbanes-Oxley Act: A New Era of Corporate Governance

In response to the Enron scandal and other corporate accounting scandals of the early 2000s, the U.S. Congress passed the Sarbanes-Oxley Act of 2002 (SOX). This landmark legislation dramatically increased corporate accountability and imposed stricter regulations on corporate governance, financial reporting, and accounting practices. Some of the key provisions of SOX include:

- Establishment of the Public Company Accounting Oversight Board (PCAOB) to oversee the audits of public companies.

- Increased penalties for corporate fraud and white-collar crime.

- Requirement for CEOs and CFOs to personally certify the accuracy of their company’s financial statements.

- Enhanced protection for whistleblowers who report corporate fraud.

- Stricter rules regarding auditor independence.

Enduring Lessons from the Enron Debacle: A Cautionary Tale for the Ages

The Enron scandal remains a stark reminder of the dangers of unchecked corporate greed, the importance of ethical leadership, and the need for robust corporate governance and regulatory oversight. It highlights the following crucial lessons:

- The Importance of Ethical Leadership: Ethical leadership is not just a nice-to-have; it’s essential for the long-term health and sustainability of any organization. A culture of integrity must start at the top and permeate every level of the company.

- The Need for Transparency and Accountability: Companies must be transparent in their financial reporting and accountable to their shareholders, employees, and the public. Opaque accounting practices and complex financial structures can be used to hide problems and mislead investors.

- The Dangers of Unchecked Ambition and Short-Term Thinking: The relentless pursuit of short-term profits at the expense of long-term sustainability can lead to disastrous consequences. Companies need to focus on creating real value, not just manipulating numbers.

- The Role of Independent Audits and Regulatory Oversight: Independent audits are crucial for verifying the accuracy of financial statements, and effective regulatory oversight is needed to protect investors and maintain market integrity.

- The Importance of Investor Skepticism: Investors need to be critical and discerning when evaluating companies. If something seems too good to be true, it probably is. Investors should carefully scrutinize financial statements and be wary of companies with overly complex structures or opaque reporting practices.

Conclusion: The Enron Legacy

The Enron scandal was a watershed moment in corporate history. It exposed the dark side of the “new economy” and shattered public trust in corporate America. While the immediate fallout was devastating, the scandal ultimately led to significant reforms that have made the financial markets more transparent and accountable. However, the Enron story remains a cautionary tale, a reminder that the temptations of greed and the allure of easy profits are ever-present. As long as these temptations exist, the need for vigilance, ethical leadership, and robust oversight will remain paramount. The Enron saga continues to serve as a powerful lesson, urging us to question, to scrutinize, and to demand accountability from those who hold positions of power and trust. The Enron story isn’t just about numbers on a balance sheet; it’s about human nature, the corrupting influence of power, and the enduring importance of integrity in a world often seduced by the illusion of easy wealth. The lessons learned from Enron’s rise and fall must not be forgotten, lest we risk repeating the mistakes of the past.

References

- Bratton, W. W. (2002). Enron and the dark side of shareholder value. Tulane Law Review, 76(5), 1275-1360. https://scholarship.law.georgetown.edu/facpub/198/

- McLean, B., & Elkind, P. (2003). The smartest guys in the room: The amazing rise and scandalous fall of Enron. Penguin.

- Thomas, W. (2002). The rise and fall of Enron. Journal of Accountancy, 193(4), 41. https://www.journalofaccountancy.com/issues/2002/apr/theriseandfallofenron.html

- Fusaro, P., & Miller, R. M. (2002). What went wrong at Enron: Everyone’s guide to the largest bankruptcy in U.S. history. John Wiley & Sons.

- Healy, P. M., & Palepu, K. G. (2003). The fall of Enron. Journal of Economic Perspectives, 17(2), 3-26. https://pubs.aeaweb.org/doi/pdfplus/10.1257/089533003765888403

- U.S. Securities and Exchange Commission. (2002). Report of Investigation in the Matter of Enron Corp. https://www.sec.gov/spotlight/enron.htm

- Sarbanes-Oxley Act of 2002, Pub. L. No. 107-204, 116 Stat. 745 (2002). https://www.govinfo.gov/content/pkg/PLAW-107publ204/pdf/PLAW-107publ204.pdf